TL;DR:

- Water damage impacts property value through repair costs, buyer hesitation stigma, and flood zone penalties. Proper documentation and professional remediation can recover much of the lost value before listing.

Water damage impact appraisal value is defined by three compounding forces: the full cost to repair physical damage, a 10%–20% stigma factor appraisers add for buyer hesitation, and location-based flood zone penalties that apply regardless of visible damage. Together, these forces can reduce a property’s appraised value far beyond what the repair bill alone suggests. Homeowners and investors who understand how appraisers calculate these deductions gain a real advantage. The right documentation and remediation approach can recover a significant portion of that lost value before a listing ever goes live.

How do appraisers quantify water damage impact on property value?

Appraisers use a method called cost-to-cure to calculate the water damage impact on a home’s appraisal. They subtract the full estimated repair cost from the property’s market value, then apply an additional adjustment for perceived risk. That second adjustment, the stigma factor, reflects buyer psychology rather than physical damage.

Appraisers subtract repair costs and then add a 10%–20% stigma reduction on top of that figure. A home worth $400,000 with $20,000 in water damage repairs could lose $20,000 in cost-to-cure plus another $38,000–$76,000 in stigma adjustments. That is a total potential loss of $58,000–$96,000 on a single water event.

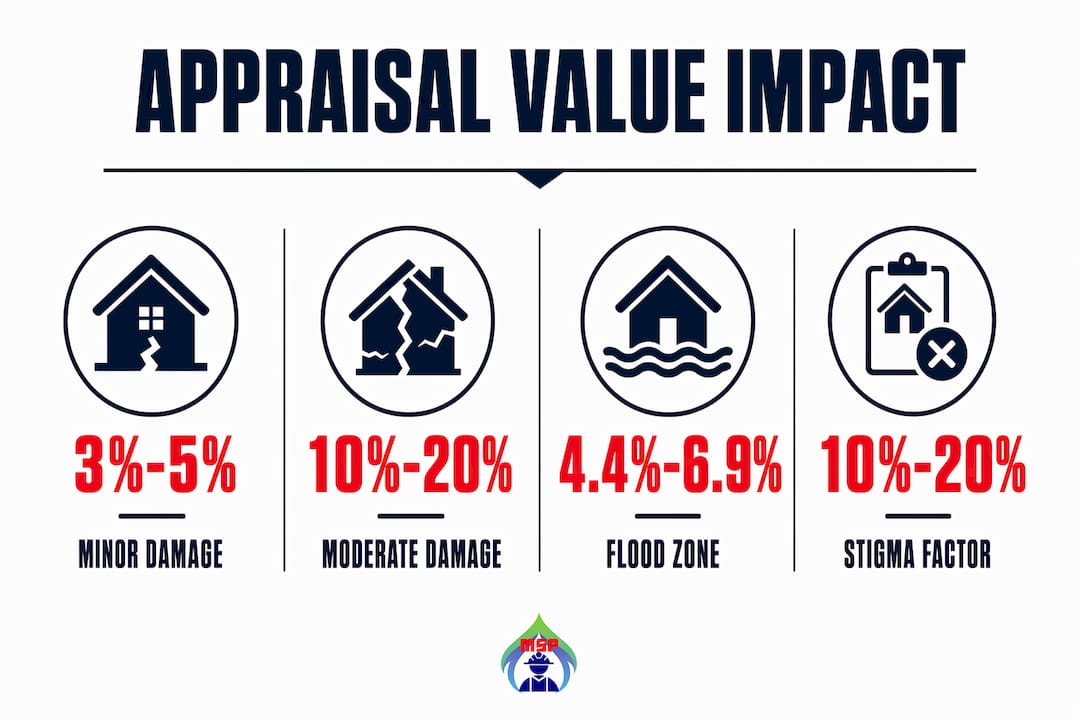

Location compounds the problem. Homes in 100-year floodplains are valued 4.4%–6.9% lower than comparable homes outside flood zones. This reduction applies even when no active damage exists, because insurance costs and perceived flood risk are baked into the appraisal.

The distinction between active and resolved damage matters significantly. Active leaks, visible mold, or standing moisture trigger the largest deductions. Fully remediated damage with professional documentation produces smaller adjustments because the appraiser can verify the condition rather than estimate worst-case scenarios.

Pro Tip: Ask your appraiser directly whether they are applying a stigma adjustment and what documentation would reduce it. Most appraisers will tell you exactly what they need.

| Damage Scenario | Typical Appraisal Impact |

|---|---|

| Minor staining, no active moisture | 3%–5% value reduction |

| Moderate damage with mold or dampness | 10%–20% value reduction |

| Severe flooding or structural damage | 30%–50% value reduction |

| Floodplain location (no visible damage) | 4.4%–6.9% automatic reduction |

| Undocumented past repairs | Treated as unverified; larger downward adjustment |

What factors influence how much value water damage removes?

Severity is the starting point for any water damage assessment. Minor cosmetic issues like ceiling stains or surface discoloration typically reduce sale price by 3%–5%. Moderate damage involving mold growth, persistent dampness, or compromised drywall pushes that range to 10%–20%. Severe flooding, structural compromise, or untreated category 3 black water can reduce sale price by up to 50%.

The quality of the repair work shapes the outcome just as much as the original damage level. A professionally completed remediation with IICRC-certified contractors, moisture clearance testing, and written documentation tells a verifiable story. An amateur patch job with no paperwork tells a story of uncertainty, and appraisers price uncertainty heavily.

Missing documentation is one of the most costly mistakes a homeowner can make. Undocumented repairs are treated as unverified by appraisers, which triggers deeper downward adjustments than the damage itself might warrant. Buyers and their lenders cannot confirm what was done, so they assume the worst.

Active moisture or mold at the time of appraisal creates a separate category of problems. These conditions can trigger FHA and VA minimum property requirement failures, which means financed buyers cannot close. That financing bottleneck either kills the deal or forces a price reduction large enough to attract a cash buyer.

Pro Tip: Get a post-remediation clearance test from an independent industrial hygienist. That single document can eliminate the majority of appraiser uncertainty about past water events.

- Minor damage (surface stains, no moisture): 3%–5% value reduction

- Moderate damage (mold, dampness, drywall): 10%–20% value reduction

- Severe damage (structural, flooding, black water): 30%–50% value reduction

- Undocumented repairs: treated as unverified, larger adjustments applied

- Active leaks or mold at appraisal: financing failures and deal cancellations

How can you minimize appraisal value loss from water damage?

The single most effective tool for protecting appraisal value is a complete remediation packet. This packet should include contractor invoices, IICRC certification documentation, moisture readings before and after drying, clearance test results, and photos of the damage at each stage of repair. Maintaining a remediation packet with IICRC-certified contractor certificates and clearance testing is the most reliable way to prevent appraiser discounts for past water damage.

Full disclosure is the second pillar of value protection. Sellers who disclose water damage history and provide repair invoices reduce the negotiation leverage buyers hold. Transparency and complete disclosure remove much of the stigma and prevent buyers from applying excessive discounts based on fear or uncertainty. Hiding damage history rarely works and creates legal liability in most states.

- Compile a full remediation packet. Gather contractor invoices, IICRC certifications, moisture logs, clearance test results, and before-and-after photos.

- Disclose the water damage history in writing. Provide a clear timeline of when damage occurred, what caused it, and how it was repaired.

- Complete all repairs before listing. Appraisers and buyers respond to finished, verified work. Partial repairs signal ongoing risk.

- Obtain a post-remediation clearance test. An independent hygienist’s clearance report removes the appraiser’s need to estimate residual risk.

- Understand your financing environment. If active moisture or mold exists, financed buyers face loan approval hurdles. Price accordingly or complete remediation first.

- Evaluate restoration versus as-is pricing. For severe damage, calculate the cost of full restoration against the expected value recovery. Sometimes a targeted repair strategy produces a better net return than full renovation.

Pro Tip: Contact your lender before listing to confirm whether the completed repairs meet FHA or VA minimum property requirements. Knowing this in advance prevents last-minute deal failures.

Understanding how long drying takes is also relevant here. Listing too soon after a water event, before materials are fully dry, creates residual moisture readings that appraisers flag immediately.

What are common appraisal pitfalls related to water damage?

Appraisers act like detectives. They focus on current documented condition and red flags like musty odors or missing documentation, which prompt larger downward adjustments. A home that smells like mildew during an appraisal walk-through will receive a stigma adjustment regardless of what the seller claims about past repairs.

Financing red flags create a separate layer of risk. Active leaks, visible mold, or moisture readings above acceptable thresholds cause financed buyers to fail inspections or lose loan approval. Water damage effects extend beyond physical repair costs to long-term financial factors including insurance, lending approvals, and resale value stability. A property that cannot support conventional financing is effectively limited to cash buyers, who typically offer significantly less.

“The uncertainty water damage creates is the main source of value loss. Clear timelines, professional repair records, and open communication can largely counteract this effect.”

Common mistakes that stall transactions include:

- Incomplete repairs that leave visible staining, odors, or soft flooring

- Lack of transparency about the damage source or repair history

- Overselling the property’s condition without documentation to back it up

- Ignoring flood zone status and its automatic impact on insurance and value

- Skipping mold inspection after water intrusion, which leaves hidden risk unaddressed

Flood zone location adds a layer that no amount of remediation can fully remove. Properties inside FEMA-designated 100-year floodplains carry mandatory flood insurance requirements. Those insurance costs reduce buyer purchasing power and suppress comparable sale prices in the area. Reviewing mold inspection red flags before listing helps identify hidden issues that would otherwise surface during the buyer’s inspection and trigger renegotiation.

Key Takeaways

Water damage reduces appraisal value through repair cost deductions, a 10%–20% stigma factor, and location-based flood zone penalties, but thorough professional remediation with complete documentation recovers the majority of that loss.

| Point | Details |

|---|---|

| Stigma factor is real and quantifiable | Appraisers add 10%–20% on top of repair costs to reflect buyer hesitation and perceived risk. |

| Severity drives the range of loss | Minor damage reduces value 3%–5%; severe flooding can cut value by up to 50%. |

| Documentation is the top value protector | IICRC-certified remediation packets with clearance tests prevent the largest appraiser discounts. |

| Flood zone location adds automatic penalties | Floodplain properties are valued 4.4%–6.9% lower regardless of visible damage. |

| Transparency reduces buyer leverage | Full disclosure with repair invoices removes the uncertainty buyers use to justify deep price cuts. |

What I’ve learned about water damage and appraisal outcomes

After working with hundreds of homeowners navigating property appraisals after floods and plumbing failures, one pattern stands out clearly: the damage itself is rarely the biggest problem. The biggest problem is the story the property tells when documentation is missing.

Buyers and appraisers are not afraid of past water damage. They are afraid of not knowing what was done about it. A home with a documented flood event, a certified remediation, and a clearance test actually sells more smoothly than a home with vague staining and no explanation. The paper trail converts fear into fact.

The second thing I’ve seen consistently is that homeowners underestimate how much lender requirements shape their options. If your property has active moisture or mold, financed buyers simply cannot close. That is not a negotiation issue. It is a loan approval issue. Fixing the problem before listing is almost always cheaper than the price reduction required to attract a cash buyer.

Savvy investors approach water-damaged properties differently. They calculate the cost of full IICRC-standard remediation, factor in the documentation value that remediation creates, and compare that against the as-is cash offer. In most cases, a properly documented restoration produces a better net return than a quick sale at a steep discount. The math usually favors doing the work right.

— John

Protect your appraisal value with professional restoration

Water damage does not have to mean a permanent loss in property value. The outcome depends almost entirely on how thoroughly the damage is addressed and how well that work is documented.

Masterservicepro provides IICRC-certified water damage restoration services across Lake County, Cook County, DuPage County, Will County, and Kane County, IL. Their technicians handle water extraction, structural drying, mold remediation, and post-remediation clearance testing under one roof. That means you get a complete, documented remediation packet from a single certified source, which is exactly what appraisers and lenders need to see. Masterservicepro backs every job with a 100% satisfaction guarantee. If you are preparing a property for appraisal or sale, getting the restoration done correctly the first time protects your investment.

FAQ

How much does water damage reduce a home’s appraisal value?

Water damage reduces appraisal value by 3%–5% for minor issues, 10%–20% for moderate damage with mold or dampness, and up to 50% for severe flooding or untreated black water. Appraisers also add a 10%–20% stigma factor on top of repair cost deductions.

Does past water damage always hurt a home appraisal?

Past water damage does not always cause major appraisal reductions if the repairs were completed by IICRC-certified contractors and documented with clearance testing. Appraisers adjust downward primarily when documentation is missing or damage appears unresolved.

Can water damage cause a buyer’s loan to be denied?

Active leaks, mold, or moisture above acceptable thresholds can cause FHA and VA appraisals to fail minimum property requirements, which blocks loan approval for financed buyers. Completing remediation before listing prevents this financing bottleneck.

Does living in a flood zone automatically lower my appraisal?

Homes inside 100-year floodplains are valued 4.4%–6.9% lower than comparable homes outside flood zones. This reduction applies regardless of visible damage because mandatory flood insurance costs and perceived risk are factored into the appraisal.

What documentation do I need to protect my appraisal after water damage?

A complete remediation packet should include contractor invoices, IICRC certification records, moisture readings before and after drying, an independent post-remediation clearance test, and photos documenting each repair stage. This packet is the most effective tool for minimizing appraiser stigma adjustments.